Valuation starts with a deceptively simple question: what is a business actually worth? A share price answers it only for a moment; reported earnings, only for a quarter. Discounted cash flow (DCF) answers it from first principles — a company is worth the present value of the cash it will generate for its owners over its remaining life.

The discipline of a DCF is that it separates price from value. Price reflects sentiment, liquidity, and the prevailing narrative; intrinsic value reflects the cash a business can actually produce and the risk attached to producing it. Most investment judgement comes down to understanding the gap between the two.

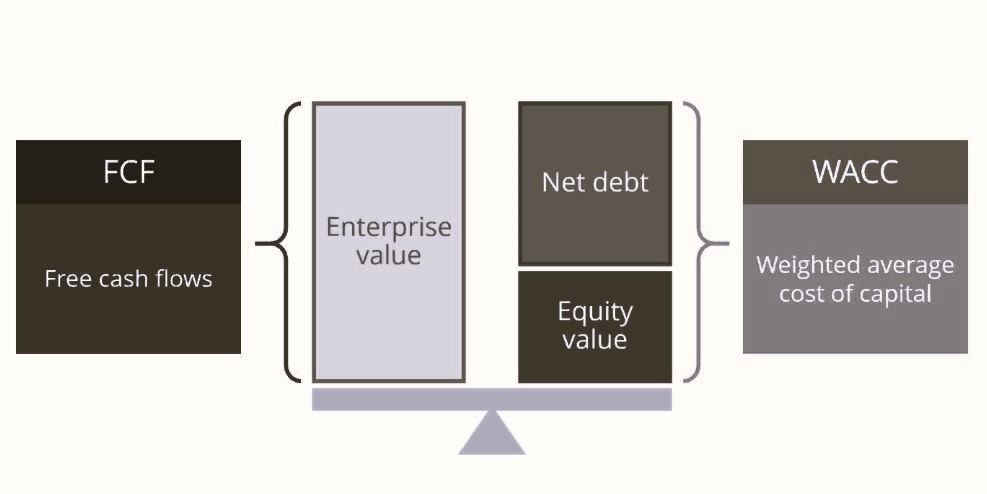

The mechanics, in four steps

- Forecast free cash flow. Project the cash the business generates after the reinvestment needed to sustain and grow it — operating profit, taxed, less investment in working capital and capital expenditure.

- Establish the discount rate. Cash received later is worth less than cash today, and riskier cash flows are discounted more heavily. The rate is the weighted average cost of capital (WACC) — the blended return debt and equity investors require to bear the risk.

- Discount the forecast to present value. Each year’s projected cash flow is restated in today’s terms and summed.

- Add the terminal value. The value of all cash beyond the explicit forecast — usually modelled as a perpetuity — is discounted to today and added to the total.

The result is intrinsic value today. Net out debt, add back cash, divide by shares outstanding, and you have a per-share figure to test against the market price.

Price reflects what the market feels. Intrinsic value reflects what the cash can support. The discipline of a DCF is keeping the two apart.

Where the disagreements live

The arithmetic is trivial; the assumptions are where valuations diverge. Two analysts applying identical mechanics can land 50% apart, because a DCF is only as defensible as its inputs. Three assumptions carry most of the weight: the revenue and margin path that drives the forecast, the discount rate (to which the output is acutely sensitive), and the terminal value — frequently more than 70% of total value, so the assumption furthest into the future tends to dominate the result. A rigorous valuation makes each one explicit and tests how far the answer moves when they change.

The one thing to remember

When you are handed a target price, the question that matters is what it assumes about growth, margins, and the discount rate. A valuation that cannot defend those three inputs is an opinion, not an analysis.

Bloom Capital Review publishes educational analysis, not investment advice.

Leave a comment