Every day on Wall Street, an unstated war is fought between two distinct tribes. In one corner sit the Number Crunchers—the disciples of the “Damodaran Doctrine”—armed with complex Discounted Cash Flow (DCF) models, Weighted Average Cost of Capital (WACC) calculations, and terminal growth rates. In the opposite corner sit the Storytellers—the architects of the “Narrative Premium”—who view spreadsheets as unimaginative cages that fail to capture the exponential reality of disruptive technology.

When valuing stable cash-flow businesses, like utilities or consumer staples, these two tribes easily find common ground. But when applied to high-growth tech firms—companies pioneering AI infrastructure, quantum computing, or space exploration—the traditional valuation toolkit often fractures completely.

The core challenge of modern corporate finance is deciding how to value an entity whose current cash flows are heavily negative, but whose narrative promises total dominance of a future macroeconomic landscape.

The Damodaran Doctrine: Translating Story into Financial Drivers

To understand this tension, we don’t have to choose between cold numbers and soaring fiction. As NYU Stern Professor Aswath Damodaran famously posits, a good valuation is simply a bridge where every story becomes a number, and every number has a story behind it.

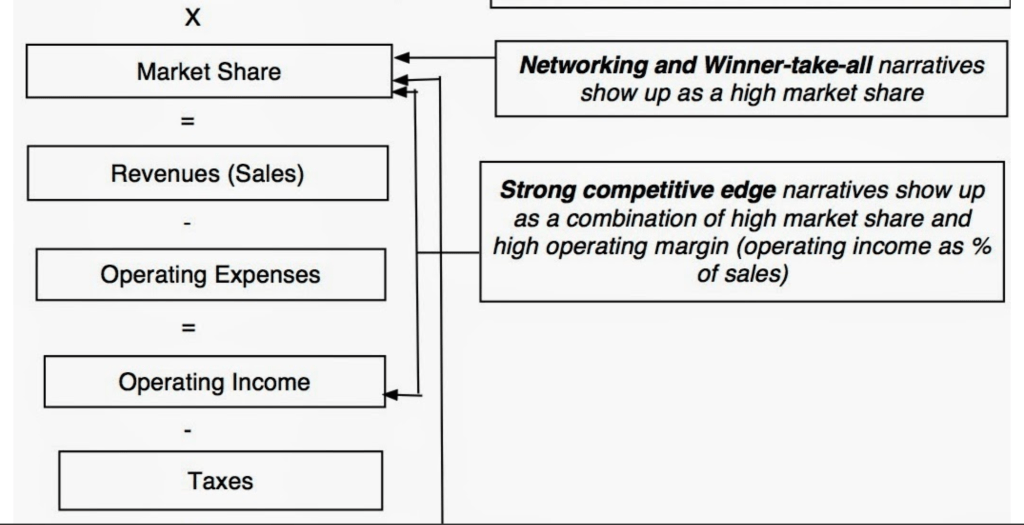

When a visionary founder pitches a narrative about a revolutionary business model, a disciplined analyst cannot simply award the company an arbitrary valuation multiple based on hype. Instead, that narrative must be systematically mapped directly to the core operational levers of corporate finance.

The Bridge from Narrative to Value Drivers. Source: Musings on Markets

When a tech firm claims a “networking, winner-take-all” advantage, that qualitative story must manifest quantitatively in a model as an expanding Market Share and accelerating Revenue Growth. If the company claims a “strong competitive edge,” it cannot simultaneously model dropping prices and shrinking margins; that edge must show up as an elevated Operating Margin that withstands competitive pressures over time.

Why Intrinsic Models Struggle with High-Growth Technology

Traditional intrinsic valuation operates on a fundamental principle: the value of an asset is the present value of its expected future cash flows, discounted at a rate that reflects its structural risk.

Intrinsic Value = Σ [ CF_t / (1 + r)^t ] + Terminal Value / (1 + r)^n

While mathematically beautiful, this formula faces distinct structural limitations when applied to early-stage or rapidly expanding tech giants for three major reasons:

- The Terminal Value Trap: For a stable company, 50% to 60% of its calculated intrinsic value comes from the “Terminal Value” (the value of cash flows beyond a 5-to-10-year forecast horizon). For a high-growth tech firm with massive current capital expenditures (CAPEX) and negative near-term free cash flow, the Terminal Value can represent 95% or more of the total valuation. This means the entire valuation is acutely sensitive to assumptions made about a distant, highly unpredictable future.

- The S-Curve Illusion: High-growth tech rarely expands in a clean, linear fashion. Growth typically follows an S-curve—sluggish initial adoption, followed by a vertical spike of geometric expansion, eventually tapering into maturity. Traditional DCF models struggle to capture these inflection points accurately, often leading to massive underpricing during the breakout phase or severe overpricing during the maturation phase.

- WACC Inelasticity: High-growth firms often carry negligible debt and are funded entirely by venture capital or volatile public equity. Calculating a cost of capital during macro regimes of shifting interest rates introduces severe estimation errors. A tiny 1% adjustment in the discount rate of a long-duration tech asset can alter its estimated intrinsic value by 30% or more.

Market Pricing and the Mechanics of the Narrative Premium

Because intrinsic models are highly sensitive to long-term inputs, public markets routinely abandon them in favor of Market Pricing. Market pricing is objective, observable, and driven entirely by current demand, liquidity, and narrative velocity.

This divergence creates the “Narrative Premium” (or, colloquially on modern trading desks, the Musk Premium). This occurs when a company’s market value completely detaches from its fundamental corporate cash flows because the market is pricing a completely different story.

| Attribute | Intrinsic Valuation (The Numbers) | Market Pricing (The Narrative) |

|---|---|---|

| Primary Driver | Cash flows, growth assets, risk metrics | Liquidity, sentiment, momentum, story |

| Time Horizon | Long-term corporate life cycle (10+ years) | Short-to-medium term catalyst windows |

| Core Tool | Discounted Cash Flows, ROIC, Capital Structure | Comparable Multiples (P/S, EV/Compute), Float |

| Systemic Risk | Underestimates disruptive shifts and optionality | Prone to severe bubbles and sudden corrections |

Consider how the market values a modern AI infrastructure firm. A traditional analyst looks at current revenue, subtracts massive data center lease costs, and struggles to justify a high valuation.

Meanwhile, the market prices the company based on a relative metric—such as Enterprise Value per cluster of advanced AI GPUs installed—under the narrative assumption that compute capacity is the new global currency. The market is not buying a multiple of trailing cash flows; it is buying a call option on a future monopoly.

The Reality Check: Possible, Plausible, and Probable

The danger of pure narrative-driven market pricing is a total loss of economic grounding, leading to market bubbles reminiscent of the dot-com era. To build a robust framework for high-growth tech valuation, analysts must run every corporate narrative through a three-tiered economic filter:

1. Is the story Possible? Does the technology violate the laws of physics or standard regulatory boundaries? If a business model relies on a technology that does not yet exist, the probability assigned to its cash flows must be near zero.

2. Is the story Plausible? Even if the technology works, does the market framework allow this narrative to exist? For example, if a ride-sharing or autonomous vehicle startup models a future revenue stream that exceeds the total aggregate GDP of the cities it operates in, the narrative is implausible.

3. Is the story Probable? This is where numbers reclaim their crown. Given the current competitive landscape, capital expenditures, and corporate execution track record, what is the actual likelihood that management can defend its competitive moat against incumbents?

The Strategic Synthesis

Ultimately, treating intrinsic valuation and narrative pricing as mutually exclusive choices is a false dichotomy. The most successful institutional investors in the technology sector do not choose between them; they utilize them in tandem.

They use the narrative to define the outer boundaries of what a company could become, capturing the massive upside of tech optionality that simple historical data hides. They then use the spreadsheet as a strict sanity check, ensuring that the market’s soaring stories don’t quietly depend on impossible margins or implausible target addressable markets.

In the fast-moving tech ecosystem of 2026, the market value of a company will always fluctuate on the whims of the current narrative. But over a long enough horizon, the story must eventually deliver the cash flows promised in the spreadsheet. The narrative gets you off the launchpad, but the numbers determine whether you stay in orbit.

Sources & References

- Damodaran, A. (2017)

. Narrative and Numbers: The Value of Stories in Business. Columbia University - Damodaran, A. (2014). “Possible, Plausible and Probable: Big Markets and Valuation.” Musings on Markets, NYU Stern.

- Mauboussin, M. J., & Callahan, D. (2021). Evaluating Moats and Technology S-Curves. Morgan Stanley Counterpoint

- Koller, T., Goedhart, M., & Wessels, D. (2020). Valuation: Measuring and Managing the Value of Companies (7th ed.). McKinsey & Company.

Leave a comment